A credit scorecard is a statistical model used by lenders to evaluate the risk of lending money to consumers. It helps in determining the creditworthiness of an individual by scoring various aspects of their financial history and current financial status. The scorecard is designed to predict the likelihood that a borrower will repay a loan on time. Start Free Trial

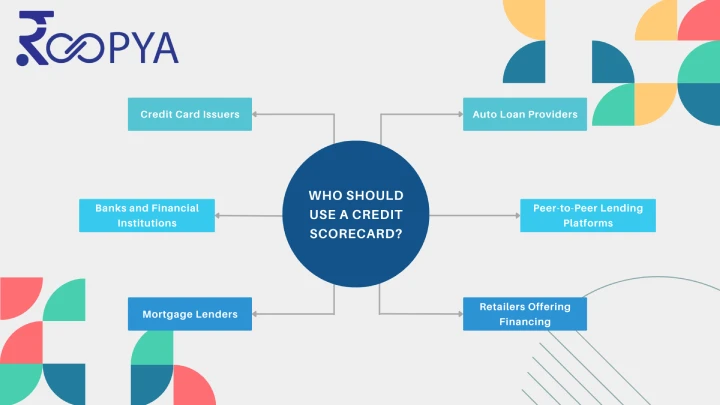

Credit scorecards are essential tools for lenders to evaluate the financial health and creditworthiness of applicants and the following type of lenders use credit scorecards:

| Lender Types | Purpose of Using Credit Scorecard |

| Banks and Financial Institutions | To assess the creditworthiness of individuals for personal loans, mortgages, or credit lines. |

| Credit Card Issuers | For evaluating applications for new credit cards and determining credit limits and interest rates. |

| Auto Loan Providers | To decide on the approval and terms of car loans, including interest rates and down payment requirements. |

| Mortgage Lenders | To evaluate the risk of lending for home purchases and set loan terms like interest rates and amounts. |

| Retailers Offering Financing | For assessing the risk of offering instalment payments or personal lines of credit to customers. |

| Peer-to-Peer Lending Platforms | To assess borrower risk profiles and set interest rates on loans funded by individual investors. |

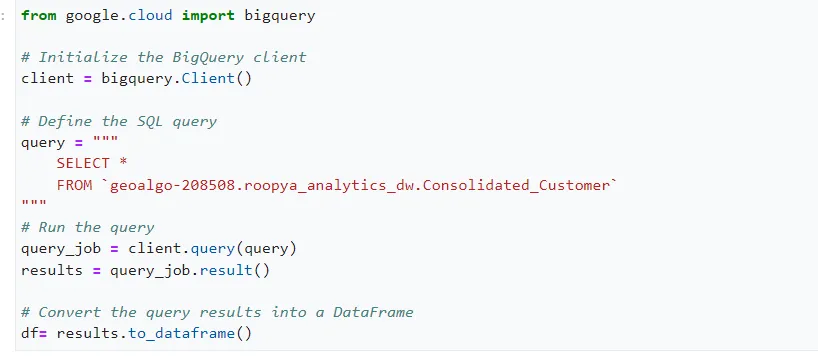

The following steps are performed at Roopya Scorecard Building process. These may vary based on product type, available parameters etc. Some sample queries are shared here.

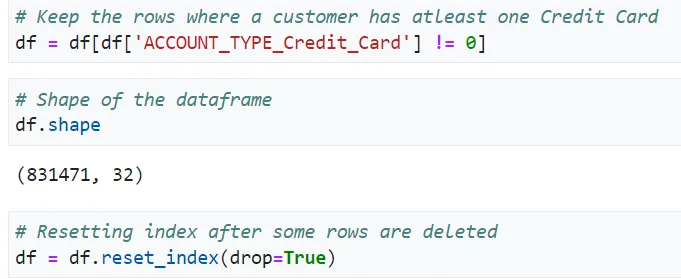

1. Extract input data from the source

2. Select the product type to create scorecard

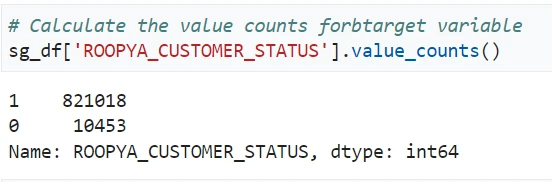

3. Define ‘Good’ / ‘Bad’ basis delinquency

4. Outlier detection and treatment

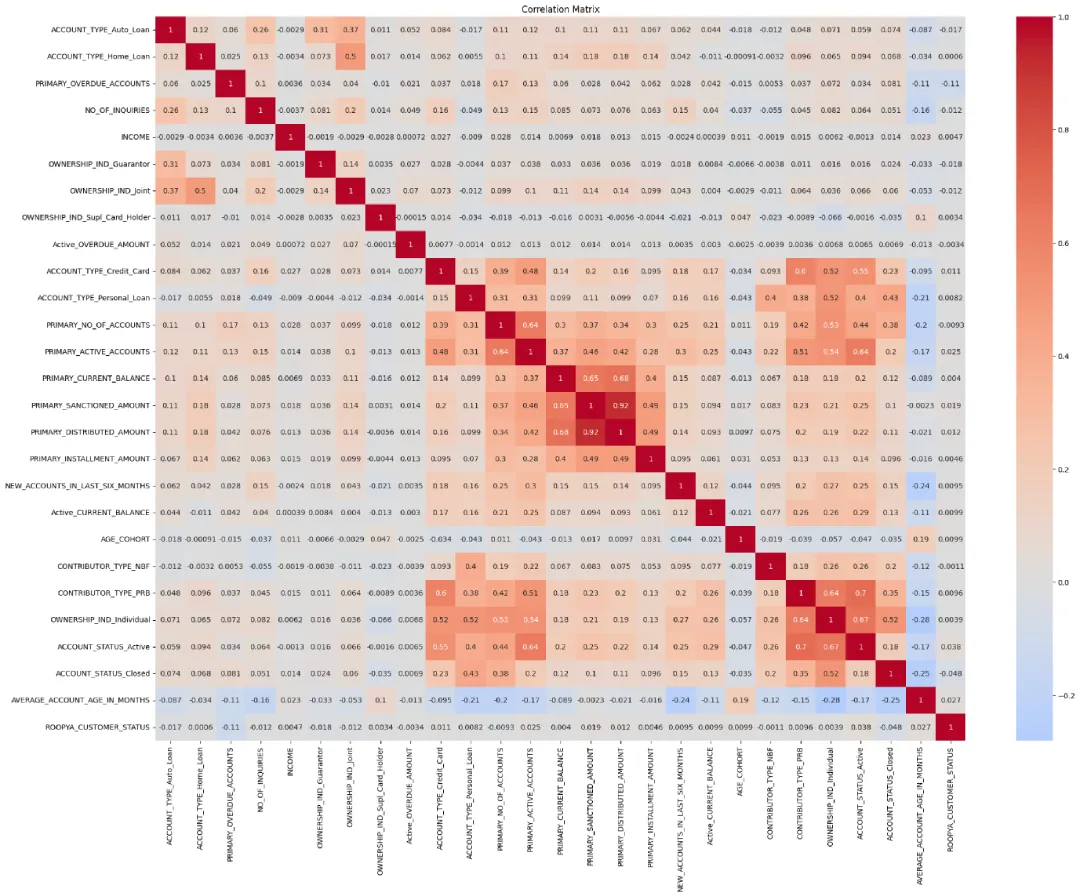

5. Correlation heatmap of features

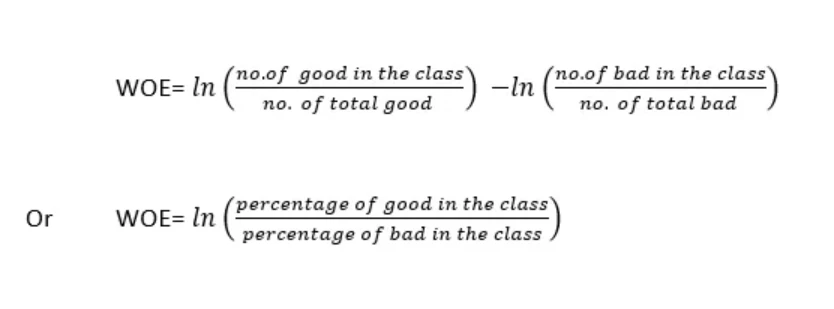

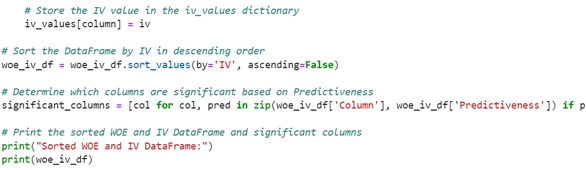

6. Weight of evidence calculation

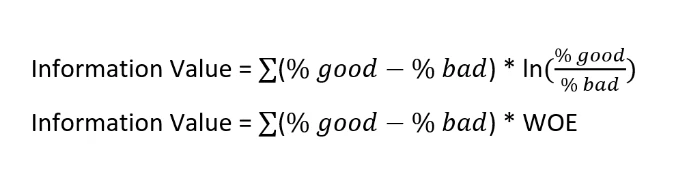

The Information Value (IV) is calculated for each column and is a measure of its ability to separate good and bad accounts. The IV for a column is the sum of IV values for all categories within that column. The formula to calculate the IV for a column is as follows

7. Predictiveness: Based on the calculated IV values, the code assigns a level of predictiveness to each column:

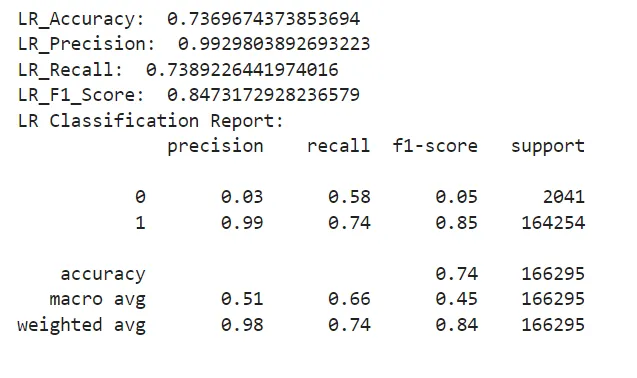

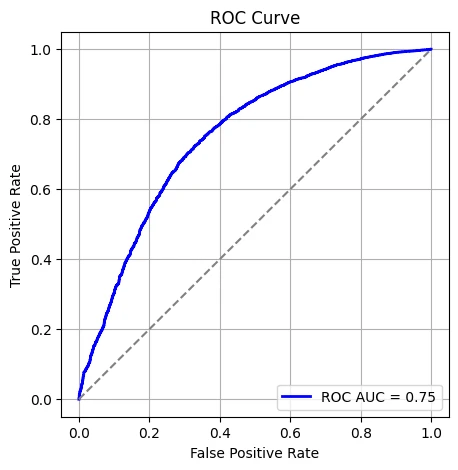

8. Evaluation metrics

Several evaluation metrics are calculated to assess the model’s performance, including:

Following determine predictive power of model:

Following determine ROC curve and ROC-AUC Score of a model

9. Generate final scorecard: We can use the scaling formula to convert predicted probabilities from logistic regression into credit scores. We can adjust the scaling parameters to fit your specific needs, such as minimum and maximum scores on a scale of 100.

These are the critical things to be taken care of while building a credit scorecard:

These are the critical things to be taken care of while building a credit scorecard:

| Consideration | Description |

| Data Quality | Ensure the data used for building the scorecard is accurate, complete, and relevant. Inaccurate or incomplete data can lead to misleading scores. |

| Regulatory Compliance | The scorecard must comply with all relevant financial regulations and laws, such as the Fair Credit Reporting Act (FCRA) and the Equal Credit Opportunity Act (ECOA), to ensure fairness and non-discrimination in lending. |

| Model Validation | Regularly validate the model to ensure its predictions are still accurate and relevant. Validation involves statistical testing and comparison against actual outcomes to assess performance. |

| Predictive Power | The scorecard should have a strong predictive power, indicating a high ability to differentiate between good and bad borrowers. This is often measured using statistics like the Gini coefficient or the area under the ROC curve (AUC). |

| Feature Selection | Carefully select features (variables) that are predictive of credit risk. Avoid variables that are not predictive or could introduce bias. Consider both traditional data (e.g., credit history) and alternative data (e.g., utility payments). |

| Bias and Fairness | Assess and minimize any biases in the scorecard that could lead to unfair treatment of certain groups of applicants. This includes ensuring the model does not unfairly penalize certain demographics. |

| Interpretability | The model should be interpretable, meaning its decisions can be understood and explained. This is important for regulatory compliance, model validation, and providing feedback to applicants who are denied credit. |

| Scalability and Efficiency | The scorecard should be able to handle the volume of applications expected, processing them efficiently without sacrificing accuracy. |

| Adaptability and Updating | Be prepared to update the scorecard over time as economic conditions, consumer behavior, and credit markets evolve. This might involve adding new variables, adjusting weights, or retraining the model with new data. |

| Transparency and Documentation | Maintain thorough documentation of the model development process, including data sources, variable selection rationale, model specifications, and validation results. This is crucial for regulatory compliance and for maintaining trust in the model. |